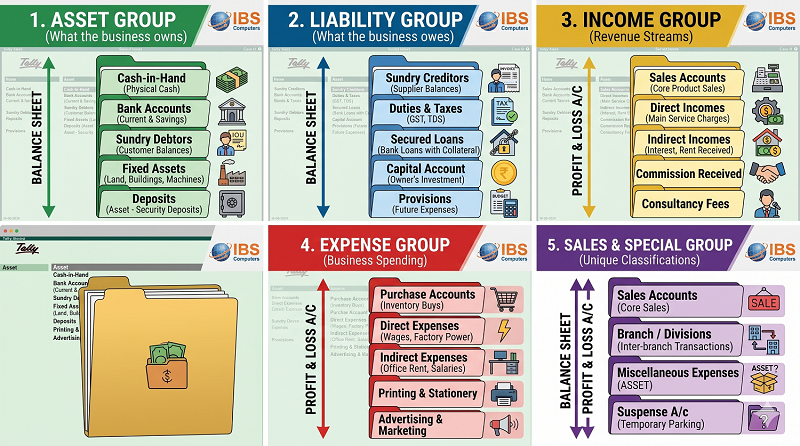

1. Asset Groups (What the business owns)

- Bank Accounts: For your standard savings or current accounts.

- Cash-in-Hand: Specifically for physical cash or petty cash ledgers.

- Current Assets: A broad category for assets that can be converted to cash within a year.

- Deposits (Asset): For security deposits (like electricity, rent, or fixed deposits).

- Fixed Assets: For long-term items like land, buildings, machinery, and furniture.

- Investments: For money put into shares, bonds, or mutual funds.

- Loans & Advances (Asset): Money you have lent to others (employees, sister concerns).

- Misc. Expenses (ASSET): Used for "Deferred Revenue Expenditure" like huge legal costs that are written off over years.

- Sundry Debtors: For customers who owe you money for goods or services sold on credit.

- Tangible: A sub-group of Fixed Assets for physical items (Assets you can touch).

2. Liability Groups (What the business owes)

- Bank OCC A/c / Bank OD A/c: Open Cash Credit or Overdraft accounts (short-term loans from banks).

- Branch / Divisions: For tracking transactions between the head office and branches.

- Capital Account: For the owner's investment (equity) and drawings.

- Current Liabilities: Debts to be paid within a year (statutory dues, bills).

- Duties & Taxes: For all tax-related ledgers like GST, VAT, or TDS.

- Loans (Liability): General group for money borrowed by the business.

- Provisions: Money set aside for known future expenses (e.g., Provision for Audit Fees).

- Reserves & Surplus: Accumulated profits kept aside for future use.

- Retained Earnings: Profit that is held back in the business instead of being distributed.

- Secured Loans: Loans taken against collateral (like a home or car loan).

- Unsecured Loans: Loans taken without collateral (like a loan from a friend).

- Sundry Creditors: Suppliers to whom you owe money for goods/services purchased.

3. Income Groups (Revenue)

- Direct Incomes: Primary revenue earned from main business activities (e.g., Service charges for a service firm).

- Income (Direct): Same as above, usually used to categorize revenue for the Trading A/c.

- Indirect Incomes: Secondary revenue not from sales (e.g., Interest received, Rent received, Commission).

- Income (Indirect): Same as above; these appear in the Profit & Loss A/c.

4. Expense Groups (Spending)

- Direct Expenses: Costs directly linked to production or purchase (e.g., Wages, Freight, Factory power).

- Expenses (Direct): These affect the "Gross Profit" in the Trading A/c.

- Indirect Expenses: Operating costs not directly linked to production (e.g., Office rent, Salary, Electricity, Printing).

- Expenses (Indirect): These affect "Net Profit" in the Profit & Loss A/c.

- Purchase Accounts: Specifically for ledgers used to buy stock/inventory.

5. Sales & Special Groups

- Sales Accounts: For ledgers used to record the sale of inventory.

- Suspense A/c: A temporary "parking spot" for transactions where the nature of the entry is unknown.

Related Post

Similar Post